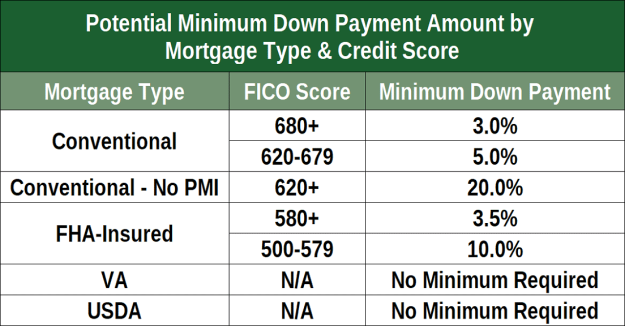

Kentucky VA Credit Score Minimum

No minimum credit score required for Kentucky VA home loan mortgages currently

Kentucky VA loans are backed by the Administration of Veterans Affairs and can be obtained with a fairly low credit score. While the VA does not set a minimum limit for credit scores, most VA-approved lenders will want to see a credit score of 620 or higher that I currently work with.

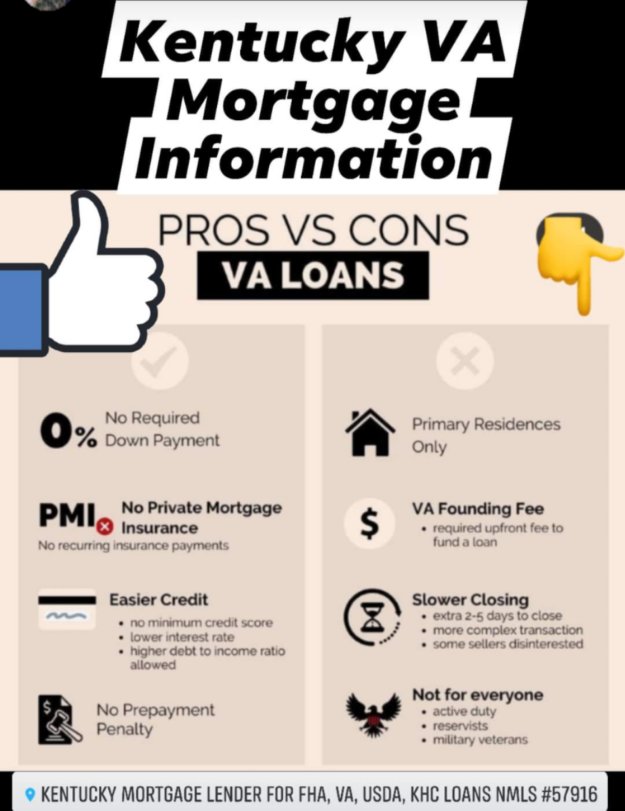

Financing to 100% of the lesser of the appraised value or sale price.

Maximum 4% seller-paid items.

Follow agency guidelines for ratio requirements and funding fee.

Related articles

- Louisville Kentucky VA Mortgage Requirements for income and debt to income ratios: (mylouisvillekentuckymortgage.com)

- Kentucky VA Loans Cash Out Requirements on a VA refinance (mylouisvillekentuckymortgage.com)

- Government shutdown affects on USDA, FHA, VA, Rural Housing, KHC and Fannie Mae Mortgage loans in Kentucky (mylouisvillekentuckymortgage.com)

- Kentucky VA Mortgage Lender Guidelines for 2020

- Kentucky VA Loans Offer 100% Financing

- Using Your Veterans Benefit to Buy a Home In Kentucky

Louisville Kentucky VA Home Loans Frequently Asked Questions

Frequently Asked Questions

- What is a COE? Where can I get one?

- COE stands for Certificate of Eligibility. This certificate proves that you are a veteran and, therefore, eligible for a VA-guaranteed home loan. Mortgage companies that work with All Military can get a COE for you during the loan process.

-

How do interest rates fluctuate?

Interest rates can change daily, sometimes even a couple times a day. They are based on the 30-year mortgage bond and many other market factors. Credit, employment status, loan program, and many other factors can also affect interest rates.

-

Why should I use my VA home loan benefit?

The VA loan program helps active duty and retired military personnel purchase homes. The VA will guarantee 100% financing on a home at a competitive rate, without you having to pay mortgage insurance. The VA also limits the types of fees that can be charged, protecting you against predatory lending.

-

What is a funding fee? Do I have to pay for this?

The VA funding fee is a fee added to loans. The Department of Veterans Affairs uses these fees to help fund its VA loan program. The first time you use a VA loan, the funding fee will be 2.15% of the loan amount. For each subsequent use, the funding fee will be 3.3%. You will be required to pay it unless you have a service-related disability of 10% or greater, in which case the funding fee is waived.

-

What does a VA lender need from me to see if I qualify for a loan?

A VA lender will want to know your income and debts, and your social security number so that your credit history can be checked. After you supply this information to a lender, it will contact you in a few hours to let you know if you are eligible for a VA loan.

-

What are the benefits of a VA loan?

A VA loan offers 100% financing with no mortgage insurance fees. The loan is assumable, and you are eligible for streamlined refinancing if rates go down. A VA loan also offers great rates and is less strict on credit than most conventional loans.

-

Can I get an interest-only loan?

Interest-only options are unavailable with VA loans. However, many VA-approved lenders offer interest-only conventional loans.

-

Can I purchase the only land with a VA loan?

No, VA loans are for home purchases and new home construction. The VA will not approve a loan that is only for land. However, you may use a VA loan to purchase a lot for a manufactured home.

-

May I use my VA eligibility more than once?

Yes, but in most cases, you can only hold one VA loan at a time. After the first home loan is paid in full, your eligibility will be restored for another loan.

-

What is the funding fee for a second VA loan?

The funding fee is 3.3 %. But with a 5% down payment, the funding fee drops to 1.5%.

-

How important is my credit score to the VA?

The VA does not emphasize credit scores as much as conventional lenders. However, it does looks for clear credit history in the borrower’s previous 12 months.

-

Can a family member use their grandparent’s or parent’s eligibility to qualify for a VA loan?

No, only a veteran or the surviving spouse of a veteran killed during active duty are eligible for VA loan benefits. Active-duty servicemembers also are eligible if the home they are purchasing will be a permanent residence and they are within 60 days of moving in.

-

Can I use a co-borrower to help get approval?

VA guidelines only allow a spouse as a co-borrower. However, many VA-approved lenders offer conventional financing, which may be more suitable if a co-borrower other than a spouse is needed to secure a loan.

-

May my spouse co-sign so that I can get a larger VA loan?

Your spouse may co-sign in order to help you qualify for a VA loan. However, your spouse’s liabilities, in addition to your spouse’s income, will be considered when determining eligibility and loan amount.

-

Can I have two VA loans at once?

No. You can have only one VA loan at a time, and it must be used for a home that is your primary residence. After you pay off that loan, you are eligible for another VA loan.

-

Does it cost anything to prequalify for a VA loan?

No, it does not. The VA loan specialists that work with VAJoe do not charge prequalification fees.

-

What are the differences between VA loans and conventional loans?

The main differences are that VA loans are guaranteed by the Veterans Administration, they require no money down, and they usually are easier to qualify for than conventional loans.

-

Are VA loan rates the same as conventional rates? Better? Worse?

Some days VA rates are better, some days they are worse. It depends on many market factors. However, VA loan rates are always close to conventional rates.

-

Does my credit score affect my VA loan rate?

No. Your credit score has no impact on VA loan rates. It can affect rates for a conventional loan.

-

If I filed for bankruptcy, can I still get a VA loan? How long must I wait after filing?

Yes, you are still eligible for a VA loan. You must be at least one year out of Chapter 13 bankruptcy or two years out of Chapter 7. You also must have no late payments in the year leading up to applying for the loan.

-

Can a friend co-sign my VA loan?

Only spouses can co-sign on VA loans. However, other loans, such as conventional home loans and FHA loans, may allow a friend to co-sign.

-

As a veteran, will my VA loan entitlement ever expire?

Your entitlement never expires. However, your Certificate of Eligibility may need to be renewed if it is older than 12 months.

-

How much can I borrow with a VA home loan?

You may be able to borrow enough to cover 100% of your home purchase and could qualify for up to a $417,000 loan. In Alaska and Hawaii, the loan guarantee limit is $625,000. On a refinance you can borrow up to 90% of the appraised value of your home.

-

May I use a VA loan to invest in real estate?

A VA loan may only be used for a home that you intend to live in as your primary residence.

-

Are VA loans provided by the U.S. government?

The Department of Veterans Affairs does not actually loan the money for VA loans. It insures loans that VA-approved lenders provide, which allows borrowers to get loan amounts for 100% of the appraised value of a home.

-

What is an adjustable-rate VA loan?

An adjustable-rate loan starts off at a slightly lower interest rate than a fixed-rate loan. Most often it stays at this rate for three, five or seven years. After that, the interest rate changes every year to the current interest rate.

-

What is a fixed-rate VA loan?

A fixed-rate loan has an interest rate that stays the same. The interest rate at the time the loan is finalized is the interest rate for the life of the loan.

-

Do I need a down payment with a VA loan?

A VA loan covers 100% of the value of a home, so a down payment is not required. However, you have to pay any closing costs. But the seller can pay these closing costs for you up to an amount that equals 6% of the home’s value. This usually is more than enough to cover closing costs, so you can move into a home with no money out of pocket.

-

May I use a VA loan for a vacation home?

No, a VA loan can only be for your primary residence.

-

If I am on active duty, can I get a VA loan?

Yes, if the home will be your permanent residence and you are within 60 days of moving in.

-

My realtor has implied that VA appraisers do poor work. Is this true?

No. VA appraisers protect buyers. VA loans are government-backed, so VA appraisers need to make sure homes meet government safety and quality guidelines

CLICK TO APPLY ONLINE

Mortgage Loan Officer

Text/call: 502-905-3708

email: kentuckyloan@gmail.com

100% LTV Financing on VA Home Loans

VA Home Loans was established to help veterans and their families obtain home financing. VA helps Servicemembers, Veterans, and eligible surviving spouses become homeowners, build, repair, retain, or adapt a home for personal occupancy.

The VA mortgage programs can be one of the most important benefits available to our Military!

Eligible properties include 1 – 2 unit primary residences, VA approved Condominium, PUDs, and Singlewide/Doublewide/Triple Wide Manufactured Housing Eligible to veterans, reservists, national guard, and surviving spouses

No down payment required!

Some restrictions may apply – See program guidelines. Lender NMLS 57916. www.nmlsconsumeraccess.org. This is not a commitment to lend. Equal Housing Lender.

Pingback: Louisville Kentucky VA Approved Condos for Jefferson County KY | KENTUCKY VA MORTGAGE LENDER

Pingback: Kentucky VA Home Loan Program – Louisville Kentucky Mortgage Loans

Pingback: Kentucky VA Mortgage Qualifications for 2021 – KENTUCKY VA MORTGAGE LENDER

What kind of credit score do you need to get a VA loan approved in Kentucky in 2019

Pingback: Kentucky VA Loan Credit Score Requirements – Louisville Kentucky Mortgage Loans