A VA mortgage loan can be a fantastic option for eligible veterans and active-duty service members looking to purchase or refinance a home in Kentucky. Understanding the qualifying criteria is crucial to navigating the process smoothly and securing the benefits offered by VA loans.

Qualifying Criteria Overview: Here’s a breakdown of the key qualifying criteria for a Kentucky VA mortgage loan:

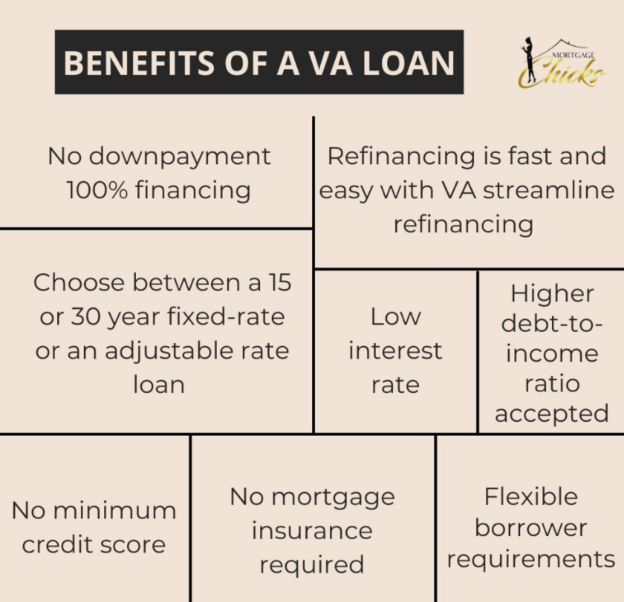

The qualifying criteria for a Kentucky VA mortgage loan in regards to income, work history, debt ratio, bankruptcy, foreclosure, time in service, loan limits, upfront funding fees, refinance, purchase, cash out refinance, down payments, property requirements in a chart or organizational chart, interest rates

| Criteria | Details |

|---|---|

| Income | Stable income that supports the ability to repay the loan. VA loans typically have more flexible income requirements. |

| Work History | A consistent 2 year work history, though exceptions can be made for veterans transitioning to civilian employment. |

| Debt Ratio | VA loans generally allow for higher debt-to-income (DTI) ratios compared to conventional loans, typically up to 41%, but can be much higher with strong credit scores, residual income, and assets |

| Bankruptcy | Generally, veterans must wait two years after a Chapter 7 bankruptcy discharge before being eligible for a VA loan. |

| Foreclosure | Veterans may be eligible for a VA loan two years after a foreclosure. |

| Time in Service | Minimum service requirements vary based on when and where the veteran served. Typically, 90 consecutive days during wartime or 181 days during peacetime are required. |

| Loan Limits | VA loan limits in Kentucky follow the conforming loan limits set by the Federal Housing Finance Agency (FHFA). |

| Upfront Funding Fees | VA loans often come with an upfront funding fee, which can vary based on factors like down payment amount, military category, and if it’s a first-time or subsequent use of the VA loan benefit. |

| Refinance Options | VA loans offer several refinancing options, including Interest Rate Reduction Refinance Loans (IRRRL) and Cash-Out Refinance loans. |

| Down Payments | VA loans are known for their zero-down payment option, making homeownership more accessible for veterans. |

| Property Requirements | VA-approved properties must meet certain standards, including being safe, sanitary, and structurally sound. |

| Interest Rates | VA loans often have competitive interest rates, which can vary based on market conditions and individual factors. |

Qualifying for a Kentucky VA mortgage loan involves meeting various criteria related to income, work history, debt ratio, military service, and more. Veterans and active-duty service members can benefit from the zero-down payment option, competitive interest rates, and flexible requirements offered by VA loans. Working with a knowledgeable mortgage professional like Joel Lobb can help navigate the VA loan process smoothly and secure the best terms possible.

Hope your day is full of sunshine

Joel Lobb Mortgage Loan Officer

American Mortgage Solutions, Inc.10602 Timberwood Circle

Louisville, KY 40223

Company NMLS ID #1364

Text/call: 502-905-3708

fax: 502-327-9119

email: kentuckyloan@gmail.com

http://www.mylouisvillekentuckymortgage.com/

NMLS ID# 57916, (www.nmlsconsumeraccess.org).

You must be logged in to post a comment.