| Exception | Maximum Loan |

|

IRRRLs |

(Lenders must use VA Form 26–8923, IRRRL Worksheet, for the actual calculation.) |

a. Does VA have Maximum Loan Amounts? |

Unlike other home loanprograms, there are no maximum dollar amounts prescribed for VA-guaranteed loans. Limitations on VA loan size are primarily attributable to two factors:1. Lenders who sell their VA loans in the secondary market must limit the size of those loans to the maximums prescribed by Government National Mortgage Association (GNMA) or whatever conduit they use to sell the loans.

2. VA limits the amount of the loan to the reasonable value of the property shown on the NOV plus the cost of energy efficiency improvements up to $6,000 plus the VA funding fee, with the following exceptions. |

Continued on next page

3. Maximum Loan, Continued

| a. Does VA have Maximum Loan Amounts? (continued) |

| Exception | Maximum Loan |

| Regular refinancing loan (cash-out) |

|

Loans to refinance are:

the veteran at an interest rate higher than that for the proposed refinancing loan. |

The lesser of:

|

| Graduated Payment Mortgage (GPM) loan on existing property |

Reference: See section 7 of chapter 7. |

| GPM loan on new home | 97.5 percent lesser of:

Reference: See section 7 of chapter 7. |

Continued on next page

3. Maximum Loan, Continued

b. Downpayment |

Because VA loans can be for the full reasonable value of the property, no downpayment is required by VA except in the following circumstances:

If a veteran has less than full entitlement available, a lender may require a downpayment in order to make the veteran a loan that meets GNMA or other secondary market requirements. The “rule of thumb” for GNMA is that the VA guaranty, or a combination of VA guaranty plus downpayment and/or equity, must cover at least 25 percent of the loan. |

4. Maximum Guaranty on VA Loans

Change Date |

April 10, 2009, Change 9

|

a. Maximum Guaranty Table |

Public Law 110-389, the Veterans’ Benefits Improvement Act of 2008, signed October 10, 2008, provided a temporary increase in the maximum guaranty for loans closed January 1, 2009 through December 31, 2011. The maximum guaranty now varies depending on the location of the property. While VA does not have a maximum loan amount, there are effective “loan limits” for high-cost counties. The limits are derived by considering both the median home price for a county and the Freddie Mac conforming loan limit. To aid lenders in determining the maximum guaranty in high-cost counties, VA has created a Loan Limitchart, with instructions. This will be updated yearly.

|

| Loan Amount | Maximum Potential Guaranty | Special Provisions |

| Up to $45,000 | 50 percent of the loan amount. | Minimum guaranty of 25 percent on IRRRLs. |

| $45,001 to $56,250 | $22,500 | Minimum guaranty of 25 percent on IRRRLs. |

| $56,251 to $144,000 | 40 percent of the loan amount, with a maximum of $36,000. | Minimum guaranty of 25 percent on IRRRLs. |

| $144,001 to $417,000 | 25 percent of the loan amount | Minimum guaranty of 25 percent on IRRRLs. |

| Greater than $417,000 | The lesser of:

|

Minimum guaranty of 25 percent on IRRRLs |

4. Maximum Guaranty on VA Loans, Continued

| a. Maximum Guaranty Table (continued) | Note: The percentage and amount of guaranty is based on the loan amount including the funding fee portion when the fee is paid from loan proceeds.For the maximum guaranty on loans for manufactured homes that are not permanently affixed (i.e., not considered real estate) see 38 U.S.C. 3712 and/or contact VA. |

5. Occupancy

Change Date |

April 10, 2009, Change 9

|

a. The Law on Occupancy |

The law requires a veteran obtaining a VA-guaranteed loan to certify that he or she intends to personally occupy the property as his or her home. As of the date of certification, the veteran must either

The above requirement applies to all types of VA-guaranteed loans except IRRRLs. For IRRRLs, the veteran need only certify that he or she previously occupied the property as his or her home.

Example: A veteran living in a home purchased with a VA loan is transferred to a duty station overseas. The veteran rents out the home. He/she may refinance the VA loan with an IRRRL based on previous occupancy of the home. |

b. What is a “Reasonable Time?” |

Occupancy within a “reasonable time” means within 60 days after the loan closing. More than 60 days may be considered reasonable if both of the following conditions are met:

Occupancy at a date beyond 12 months after loan closing generally cannot be considered reasonable by VA. |

Continued on next page

5. Occupancy, Continued

c. When Can a Spouse Satisfy the Occupancy Requirement? |

Occupancy (or intention to occupy) by the spouse satisfies the occupancy requirement for a veteran who is on active duty and cannot personally occupy the dwelling within a reasonable time.Occupancy by the spouse may satisfy the requirement if the veteran cannot personally occupy the dwelling within a reasonable time due to distant employment other than military service. In these specific cases, consult your Regional Loan Center (RLC) to determine if this type of occupancy meets VA requirements.Note: The cost of maintaining separate living arrangements should be considered in underwriting the loan.

For an IRRRL, a certification that the spouse previously occupied the dwelling as a home will satisfy the requirement. No family member or person other than the veteran’s spouse can satisfy the occupancy requirement for the veteran. |

d. Occupancy Requirementsfor DeployedActive Duty Servicemembers |

Single or married servicemembers, while deployed from their permanent duty station, are considered to be in a temporary duty status and able to meet the occupancy requirement. This is true without regard to whether or not a spouse will be available to occupy the property prior to the veteran’s return from deployment. |

e. Occupancy After Retirement |

If the veteran states that he or she will retire within 12 months and wants a loan to purchase a home in the retirement location

– Include a copy of the veteran’s application for retirement submitted to his or her employer.

– If retirement income alone is insufficient, obtain firm commitments from an employer that meet the usual stability of income requirements. Note: Only retirement on a specific date within 12 months qualifies. Retirement “within the next few years” or “in the near future” is not sufficient. |

Continued on next page

5. Occupancy, Continued

f. Delayed Occupancy Due to Property Repairs or Improvements |

Home improvements or refinancing loans for extensive changes to the property which will prevent the veteran from occupying the property while the work is being completed, constitute exceptions to the “reasonable time” requirement. The veteran must certify that he or she intends to occupy or reoccupy the property as a home upon completion of the substantial improvements or repairs. |

g. Intermittent Occupancy |

The veteran need not maintain a physical presence at the property on a daily basis. However, occupancy “as the veteran’s home” implies that the home is located within reasonable proximity of the veteran’s place of employment. If the veteran’s employment requires the veteran’s absence from home a substantial amount of time, the following two conditions must be met:

Use of the property as a seasonal vacation home does not satisfy the occupancy requirement. |

h. Unusual Circumstances |

Discuss unusual circumstances of occupancy with the appropriate VA office or submit a description of the circumstances to the VA office for prior approval. |

Continued on next page

5. Occupancy, Continued

i. The Certification |

The veteran certifies that the occupancy requirement is met by checking the appropriate occupancy block and signing:

This satisfies the lender’s obligation to obtain the veteran’s occupancy certification. The lender may accept the occupancy certification at face value unless there is specific information indicating the veteran will not occupy the property as a home or does not intend to occupy within a reasonable time after loan closing. Where doubt exists, the test is whether a reasonable basis exists for concluding that the veteran can and will occupy the property as certified. Contact the appropriate VA office if the lender cannot resolve issues involving the veteran’s intent by applying this test. |

6. Interest Rates

Change Date |

April 10, 2009, Change 9

|

a. Requirement |

VA no longer prescribes interest rates for VA-guaranteed loans. The interest rate is negotiated between the veteran-borrower and the lender to allow the veteran to obtain the best available rate. |

b. Changes to the Agreed Upon Interest Rate |

The lender and borrower are expected to honor any lock-in or other agreements they have entered into which impact the interest rate on the loan. VA does not object to changes in the agreed upon rate, as long as no lender/borrower agreements are violated. The following procedures apply in such cases.Any increase in the interest rate of more than one percent requires

Reference: For prior approval loans, see section 4 of chapter 5. |

7. Discount Points

Change Date |

April 10, 2009, Change 9

|

a. Requirement |

Veterans may pay reasonable discount points on VA-guaranteed loans. The amount of discount points is whatever the borrower and lender agree upon. Discount points can be based on the principal amount of the loan after adding the VA funding fee, if the funding fee will be paid from loan proceeds. |

b. When Can Points be Included in the Loan? |

Discount points may be rolled into the loan only in the case of refinancing loans, subject to the following limitations:Interest Rate Reduction Refinancing Loans A maximum of two discount points can be rolled into the loan.

If the borrower pays more than two points, the remainder must be paid in cash. Refinancing of Construction Loans, etc. Loans to refinance are:

Any reasonable amount of discount points may be rolled into the loan as long as the sum of the outstanding balance of the loan plus allowable closing costs and discount points does not exceed the VA reasonable value. Reference: See the maximum loan limitations in section 3 of this chapter. Cash-out Refinancing Loans While discount points cannot specifically be included in the loan amount, the borrower can receive cash from loan proceeds, subject to maximum loan limits (See section 3 of this chapter). The cash received by the borrower can be used for any purpose acceptable to the lender, including payment of reasonable discount points. |

Continued on next page

- Discount Points, Continued

c. Changes to the Agreed Upon Discount Points |

The lender and borrower are expected to honor any agreements they have entered into which impact the discount points paid on the loan. VA does not object to changes in the agreed upon points, as long as no lender/borrower agreements are violated. The following procedures apply in such cases.Any increase in discount points requires

Reference: For prior approval loans, see section 4 of chapter 5. |

8. Maturity

Change Date |

April 10, 2009, Change 9

|

a. Maximum Maturity |

In addition, every loan must be repayable within the estimated economic life of the property securing the loan. The period for repayment of a loan is measured from the date of the note or other evidence of indebtedness. |

b. Maturity Extending Beyond the Maximum |

VA regulations provide that any amounts, which fall due beyond the maximum maturity automatically, fall due on the maximum maturity date. Thus, if a lender inadvertently makes a loan that exceeds the maximum maturity, it may still be subject to guaranty.However, the regulations also limit the amount that can be collected as a final installment, such as, they prohibit excessive ballooning. The holder of a loan that violates this provision may desire to correct the situation through means which are legally proper in the jurisdiction. |

9. Amortization

Change Date |

April 10, 2009, Change 9

|

a. Requirement |

All VA loans must be amortized if the maturity date is beyond 5 years from the date of the loan. Loans with terms less than 5 years are considered term loans and need not be amortized.Generally, for amortized VA loans:

Exceptions to these requirements are made in the case of |

b. Alternative Amortization Plans |

Certain amortization plans which do not meet the requirements described in section a above may be used if approved in advance by VA. A lender may submit an amortization plan to VA for prior approval if the plan:

Exception: GPMs and GEMs. |

Continued on next page

9. Amortization, Continued

c. Special Provisions for Construction Loans |

See “Amortization” in section 2 of chapter 7. |

d. Standard and Springfield Plans |

The Standard and Springfield plans satisfy VA amortization requirements.

|

10. Eligible Geographic Locations for the Secured Property

Change Date |

April 10, 2009, Change 9

|

a. Where Can the Property be Located? |

Real property securing a VA-guaranteed loan must be located in the United States, its territories, or possessions (Puerto Rico, Guam, Virgin Islands, American Samoa and the Northern Mariana Islands). |

11. What Does a VA Guaranty Mean to the Lender?

Change Date |

April 10, 2009, Change 9

|

a. Protection Against Loss |

VA guarantees a portion of the loan, identified on the VA Loan Guaranty Certificate (LGC) by percentage and dollar amounts. If a loss ultimately occurs on the loan, VA will reimburse the loan holder for all or part of such loss

|

b. Lender Responsibility |

It is the lender’s responsibility to comply with all laws and regulations related to the VA Loan Guaranty Program, and thereby prevent VA’s denial or reduction of a payment on a future claim. A lender can accomplish this by ensuring that its employees who perform work related to VA lending

|

c. When is a Loan that was Closed Automatically Guaranteed? |

A loan is automatically guaranteed by VA upon closing (prior to issuance of the LGC) provided the loan was made by

|

Continued on next page

11. What Does a VA Guaranty Mean to the Lender?, Continued

d. When is a Prior Approval Loan Guaranteed? |

A prior approval loan is also guaranteed by VA upon closing (prior to issuance of the LGC) provided

|

e. What is Evidence of Guaranty? |

Evidence of guaranty is VA Form 26-1899, Loan Guaranty Certificate, which is generated electronically via VA’s webLGY application. The LGC represents tangible proof to the lender that VA’s guaranty is given in good faith. It is contingent upon:

For example, VA may deny or reduce payment on a future claim based on the lender or holder’s noncompliance whether or not VA has issued evidence of guaranty on the loan. The LGC also has an audit indicator that, if noted Yes, lets the lender know the case has been identified for full review. In these instances, the lender then needs to submit a complete loan origination package to the appropriate VA office for review. Packages should be submitted within 15 days of the LGC being generated. |

f. Total Loss of Guaranty |

Willful fraud or material misrepresentation by the lender or holder, or by an agent of either, will relieve VA of liability for payment of any claim on the loan. VA also has no liability in the case of

A holder of a VA loan who acquired the loan without notice or knowledge of fraud or material misrepresentation in procuring the guaranty will not be denied payment of any claim on the loan by reason of such fraud or material misrepresentation. |

Continued on next page

11. What Does a VA Guaranty Mean to the Lender?, Continued

g. Partial Loss of Guaranty |

A holder of a VA loan who fails to comply with applicable laws and regulations may receive only partial payment of a claim if VA’s liability increases due to the holder’s noncompliance. Material misrepresentation which is not willful has the same consequence.No claim will be paid on such loan until the amount of any increase in VA’s liability is known. The burden of proof is on the holder to establish that VA’s increased liability is not due to the holder’s noncompliance or misrepresentation.Examples of noncompliance with applicable law and regulations which may lead to an increase in VA’s liability include:

|

12. Post-Guaranty Issues

Change Date |

April 10, 2009, Change 9

|

a. Corrections to LGCs |

LGCs are generated using data entered from several sources, including the VA Funding Fee Payment System (VA FFPS). If a lender discovers an error in reported data, such as date of loan closing, beforethey have generated the LGC, they must access the VA FFPS system to make the correction. This will then result in the correct closing date being shown when the LGC is obtained. If the error is discovered after the LGC has been generated, lenders will need to contact the appropriate VA RLC for assistance. An LGC with minor typographical errors that do not compromise accurate identification of the loan is valid. |

b. Replacement of Missing LGC with Duplicate |

A lender may obtain duplicate LGCs at any time simply by accessing the system and reprinting the LGC. |

c. Transfer of Loans |

It is not necessary to notify VA of the assignment of a guaranteed loan. |

d. Loan Assumptions |

The assumption of VA-guaranteed loans for which commitments were made on or after March 1, 1988, requires the approval of VA (or certain lenders on VA’s behalf). |

Continued on next page

12. Post-Guaranty Issues, Continued

e. Paid-in-Full Loans |

Holders of VA-guaranteed loans are required to electronically report the date the loan was paid-in-full in the VA Loan Electronic Reporting Interface (VALERI) system. Lenders are required to report paid-in-full loans to VA upon full satisfaction of the loan by payment or otherwise. Lenders/servicers are not required to mail LGCs to VA when a loan is terminated. Since this information will now be reported through VALERI, there is no need to have the actual LGC returned to VA upon termination of the loan. |

f. Maintenance of Loan Records |

Lenders must maintain copies of all loan origination records onVA-guaranteed home loans for at least 2 years from the date of loan closing. Even if the loan is sold, the original lender must maintain these records (or legible copies) for the required period.Loan origination records include:

Lenders must make these records accessible to VA personnel conducting audit reviews. |

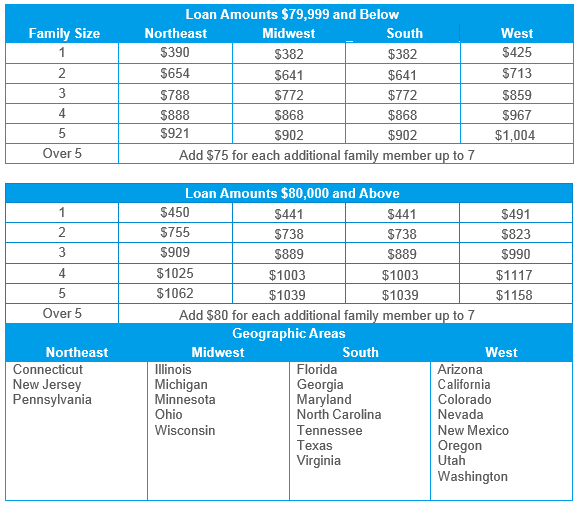

| Residual Income for a Kentucky VA Loan Approval |

Residual income is the amount of income remaining after housing expenses, income taxes, long-term obligations and other expenses have been deducted from the borrower’s total gross pay. VA requires a specific amount of monthly residual income be available for the borrower’s use. This amount is based on the family size, location of the property and loan amount.

|

—

Senior Loan Officer

502-905-3708 cell

kentuckyloan@gmail.com

http://www.mylouisvillekentuckymortgage.com/

Pingback: Louisville Kentucky VA Approved Condos for Jefferson County KY | KENTUCKY VA MORTGAGE LENDER

Pingback: Kentucky VA Home Loan Program – Louisville Kentucky Mortgage Loans

Pingback: Kentucky VA Mortgage Loan Guide for Foreclosures, Bankruptcy, and short sales or deed in lieu. – Louisville Kentucky Mortgage Loans

RECENT POSTS

First Time Home Buyer Qualifications in Kentucky.

VA Home Loan Advantages

Kentucky VA Loans for Kentucky First-Time Home Buyers

Kentucky VA Loan Refinance and Purchase Guidelines

Kentucky VA Homes for Sale- Kentucky VA Assumable Mortgages

Pingback: Kentucky VA Loan Guidelines – Louisville Kentucky Mortgage Loans

Pingback: Kentucky VA Loan Guidelines | Louisville Kentucky Mortgage Loans

I enjoy your work , thanks for all the useful articles .

Pingback: Louisville Kentucky VA Mortgage « Kentucky VA Mortgage Home Lender

I am they wouldappy that I observed this site , the ideal info that I was looking for!