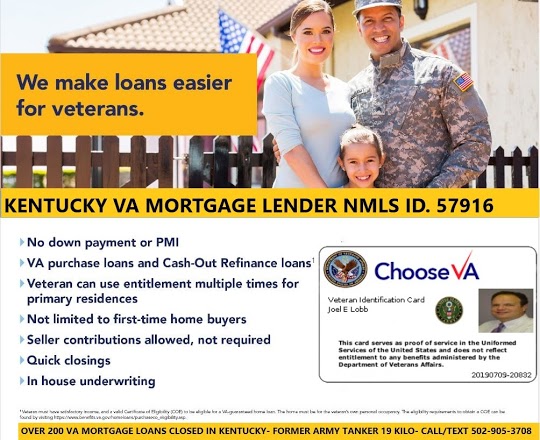

Kentucky VA Loan Benefits

No Minimum Credit Score

No private mortgage insurance (PMI)

No pre-payment penalty

VA regulation limits closing costs

Sellers can pay all closing costs up to 4% of the sales price to include veteran’s debt obligations.

Kentucky VA Mortgage does not have a minimum credit score requirement. When a lender requires a minimum credit score it is generally a 580-620, that is called a lender overlay. An overlay is a lender’s own underwriting guidelines above and beyond the VA guidelines.

The most common reason for a Veteran’s loan to be declined is not having a required minimum credit score per the lenders own set of guidelines above and beyond what the VA requires.

As announced by the VA in Circular 26-19-30 (which provides interim guidance on implementing “The Blue Water Navy Vietnam Veterans Act of 2019″) the conforming loan limit cap on guarantees was removed for Veterans with full entitlement. For Veterans who have previously used entitlement and the entitlement has not been restored, the maximum amount of guaranty entitlement available to the Veteran (for a loan above $144,000) is 25 percent of the conforming loan limit reduced by the amount of entitlement previously used (not restored) by the Veteran. The new guaranty requirements apply for loans closed on or after January 1, 2020.

In 1944, the Servicemen’s Readjustment Act was established in to provide veterans and their surviving spouses with a number of benefits. Among these benefits was the VA loan program. VA loans allow veterans and military to purchase homes with 100% financing, no mortgage insurance, and limited closing costs.

In order to apply for a VA loan, you need to meet eligibility requirements. Most veterans, military, and spouses of deceased military members will be eligible. Veterans can apply without any delay if minimum active duty service requirements have been met. Active duty service members on the other hand will need to complete a minimum of 6 months of service first. National Guard and reservists will need to wait 6 years before the benefit kicks in. If they are called to active duty at any point, they will become eligible after only 181 days.

Anyone who intends to apply for a VA loan will need to obtain their Certificate of Eligibility. It is important to note that the COE only proves to your lender that you have met the minimum service requirements. It is not a guarantee that you will be approved for a loan. One of the easiest ways to get your COE is through the VA’s eBenefits Portal. Whether you are looking to purchase your very first home or are looking to take advantage of the VA loan program to refinance, we can help you find a loan that meets your exact needs.

—

http://www.benefits.va.gov/homeloans

6 STEPS IN ARRANGING A VETERAN’S GUARANTEED LOAN

1. Find the property suitable for your needs.

2. Go to a lender and apply for the loan.

3. Present your discharge or separation papers relating to latest period of service and/or a

Certificate of Eligibility.

4. Property is appraised by approved appraiser.

5. Estimate of property’s reasonable value is determined.

6. If application is approved, you get the loan.

WHAT VA CAN DO

VA loans offer the following important features:

Ensure that all veterans are given an equal opportunity to buy homes with VA assistance,

without regard to their race, color, religion, sex, handicap, familial status, or national origin;

No down payment (unless required by the lender, the purchase price is more than the

reasonable value of the property as determined by VA, or the loan is made with graduated

payment features);

A freely negotiable fixed interest rate competitive with conventional mortgage interest rates;

The buyer is informed of the estimated reasonable value of the property;

• Limitations on closing costs;

An assumable mortgage. However, for loans closed on or after March 1, 1988, the

assumption must be approved in advance by the lender or VA. Generally, this involves a

review of the creditworthiness of the purchaser (ability and willingness to make the mortgage

payments). Be sure to see section entitled “Loan Repayment Terms”;

Long amortization (repayment) terms;

Right to prepay without penalty (lenders may require that any partial prepayments be in the

amount of at least 1 monthly installment of principal or $100, whichever is less);

For houses inspected by VA during construction, a warranty from the builder and VA

assistance in trying to obtain the builder’s cooperation in correcting any justified construction

complaint; and

Forbearance extended to VA homeowners experiencing temporary financial difficulty.

WHAT VA CANNOT DO

GUARANTEE THAT THE HOUSE YOU BUY, WHETHER IT IS NEW OR PREVIOUSLY

OCCUPIED, WILL BE FREE OF DEFECTS. The VA appraisal is NOT intended to be an

“inspection” of the property. It is in your best interest to seek expert advice BEFORE you

legally commit yourself in a purchase agreement, particularly if you have any doubts about

the condition of the house. Most sellers will permit you, at your expense, to arrange for an

inspection by a qualified residential inspection service and negotiate with you concerning

repairs to be included in the purchase agreement. Such action can prevent later problems,

disagreements and disappointments.

Remember, VA guarantees only the loan, NOT the condition of the property. It is your

responsibility to be an informed buyer and assure yourself that what you are buying is

satisfactory to you in all respects.

If you have a home built, VA cannot compel the builder to correct construction defects or

otherwise live up to the contract. VA authority is limited to suspension of the builder from

participation in the VA Loan Guaranty program.

VA cannot guarantee that you are making a good investment or that you can resell the house

at the price you paid.

VA does not have the authority to provide you with legal services.

REQUIREMENTS FOR VA LOAN APPROVAL

To get a VA loan the law requires that:

You must be an eligible veteran who has available home loan entitlement (except in the case

of an interest rate reduction refinancing loan–see “Interest Rates” below.

The loan must be for an eligible purpose. The purchase price should not exceed the

appraised value. Otherwise, you will have to pay the difference from your own resources;

You must occupy or intend to occupy the property as your home within a reasonable period of

time after closing the loan;

You must have enough income to meet the new mortgage payments on the loan, cover the

costs of owning a home, take care of other obligations and expenses, and still have enough

income left over for family support (a spouse’s income is considered in the same manner as

the veteran’s); and

• You must have a good credit record.

THE GUARANTY

VA-guaranteed loans are made by private lenders such as banks, savings and loan associations,

or mortgage companies. To get a loan, you apply to the lender. If the loan is approved, VA

guarantees the loan when it is closed. The guaranty means the lender is protected against loss if

you or a later owner fail to repay the loan.

Questions and Answers

1. How much is the guaranty?

VA will guarantee up to 50 percent of a home loan up to $45,000. For loans between $45,000

and $144,000, the minimum guaranty amount is $22,500, with a maximum guaranty, of up to 40

percent of the loan up to $36,000, subject to the amount of entitlement a veteran has available.

For loans of more than $144,000 made for the purchase or construction of a home or to purchase

a residential unit in a condominium or to refinance an existing VA-guaranteed loan for interest

rate reduction, the maximum guaranty is the lesser of 25% or $104,250 which is 25% of the

Freddie Mac conforming loan limit for a single family residence for 2007. This figure will change

yearly. (For information about entitlement see “Service Eligibility” below.)

2. Is $36,000 the biggest loan a veteran can get?

No. You may generally borrow up to the reasonable value of the property or the purchase price,

whichever is less, plus the funding fee, if required. For certain refinancing loans, the maximum

loan is limited to 90 percent of the value of the property, plus the funding fee, if required. To

determine the reasonable value, VA requires an appraisal of the property. (Also see

“Downpayment Requirements” below.

3. What is the maximum VA loan?

There is no maximum VA loan, except that the loan cannot exceed the lesser of the appraised

value or purchase price, plus VA funding fee and energy efficient improvements, if applicable.

However, lenders usually won’t make a no-downpayment loan larger than $ ($625,500 in

Alaska, Hawaii, Guam, and U.S. Virgin Islands) due to secondary market limitations.

4. Must the loan be repaid?

Yes. A VA guaranteed loan is not a gift. It must be repaid, just as you must repay any money

you borrow. The VA guaranty, which protects the lender against loss, encourages the lender to

make a loan with terms favorable to the veteran. But if you fail to make the payments you agreed

to make, you may lose your home through foreclosure, and you and your family would probably

lose all the time and money you had invested in it. If the lender does take a loss, VA must pay

the guaranty to the lender, and the amount paid by VA must be repaid by you. If your loan closed

on or after January 1,1990, you will owe the Government in the event of a default only if there

was fraud, misrepresentation, or bad faith on your part.

5. Does VA make any loan directly to eligible veterans?

Yes, but only to Native Americans on trust land or to supplement a grant to get a specially

adapted home for certain eligible veterans who have a permanent and total service-connected

disability(ies). For information concerning direct loans to Native American Veterans see VA

Pamphlet 26-93-1, which can be found on the internet at: http://www.benefits.va.gov/homeloans/vap26-

93-1.asp. See VA Pamphlet 26-69-1 for information concerning specially adapted housing

grants.

SERVICE ELIGIBILITY

You are eligible for VA financing if your service falls within any of the following categories:

Wartime Service. If you served any time during:

World War II (September 16, 1940 to July 25, 1947),

Korean Conflict (June 27, 1950 to January 31, 1955),

Vietnam Era (August 5, 1964 to May 7, 1975), the Vietnam Era begins February 28,

1961 for individuals who served in the Republic of Vietnam.

Persian Gulf War (August 2, 1990 to present (requires service for 2 years or the full

period for which called to active duty, except that exceptions applying to service

between September 7, 1980 and August 1, 1990 also apply to Persian Gulf War).)

See below.

You must have served at least 90 days on active duty and been discharged or released under

other than dishonorable conditions. If you served less than 90 days, you may be eligible if

discharged because of a service-connected disability.

Peacetime Service. If your service fell entirely within any one of the following periods:

July 26, 1947 to June 26, 1950,

February 1, 1955 to August 4, 1964, or

May 8, 1975 to September 7, 1980 (if enlisted) or to October 16, 1981 (if officer, you

must have served at least 181 days of continuous active duty and been discharged or

released under conditions other than dishonorable). If you served less than 181 days,

you may be eligible if discharged because of a service-connected disability.

Service between September 7, 1980 (enlisted) or October 16, 1981 (officer) and

August 1, 1990.

If your entire period of service was between September 7, 1980 (October 16, 1981) and

August 1, 1990, you must have:

Completed 24 months of continuous active duty or the full period (at least 181 days) for which

you were called or ordered to active duty, and been discharged or released under conditions

other than dishonorable.

You may also be determined eligible if you were discharged for a service-connected disability,

or you were discharged for the convenience of the Government after completing at least 20

months of a 2-year enlistment, or you completed 181 days of active duty and:

were discharged because of a hardship, or

were determined to have a service-connected compensable disability, or

were discharged or released from active duty for a medical condition which preexisted service

and has not been determined to be service-connected, or

If the certificate cannot be issued by ACE, you can request it from VA, by completing VA Form

26-1880, “Request for A Certificate of Eligibility.” The form should be submitted along with either

• received an involuntary discharge or release from active duty for the convenience of the

Government as a result of a reduction in force, or

were discharged or released from active duty for a physical or mental condition not

characterized as a disability and not the result of misconduct, but which did interfere with your

performance of duty.

NOTE: During the Persian Gulf War, the foregoing exceptions to the 2-year requirement apply,

except that 90 days of active duty is sufficient in lieu of 181 days.

Active Duty Service Personnel. If you are now on active duty, eligibility can be established

after having served on continuous active duty for at least 90 days. Upon discharge or release

from active duty, eligibility must be reestablished.

Members of the Selected Reserve. Individuals who are not otherwise eligible and who have

completed at least 6 years in the Reserves or National Guard, or been discharged because of a

service-connected disability, and

have been discharged with an honorable discharge, or

have been placed on the retired list, or

have been transferred to an element of the Ready reserve other than the

Selected Reserve, or

continue to serve in the Selected Reserve are eligible for a GI loan.

Other Types of Service

Certain United States citizens who served in the armed forces of a government allied with the

United States in World War II.

Unmarried surviving spouses of the above-described eligible persons who died as the result

of service or service-connected injuries (Children of deceased veterans are not eligible).

NOTE: Also, a surviving spouse who remarried on or after attaining age 57, and on or after

December 16, 2003, may be eligible for the home loan benefit.

The spouse of any member of the Armed Forces serving on active duty who is listed as

missing in action, or is a prisoner of war and has been so listed for a total of more than 90

days.

Individuals with service as members in certain other organizations, services, programs and

schools may also be eligible. Questions about whether this service qualifies for home loan

benefits should be referred to your VA Regional Loan Center.

Obtaining a Certificate of Eligibility

VA determines your eligibility and, if you are qualified, a Certificate of Eligibility will be issued.

ACE (automated certificate of eligibility): In some cases veterans can obtain the Certificate of

Eligibility from a lender. Most lenders have access to the ACE system. This Internet based

application can establish eligibility and issue an online Certificate of Eligibility in a matter of

seconds. Not all cases can be processed through ACE – only those for which VA has sufficient

data in our records. However, veterans are encouraged to ask their lenders about this method of

obtaining a certificate.

the originals or legible copies of your most recent discharge or separation papers covering active

military duty since September 16, 1940, which show active duty dates and type of discharge.

This form may be obtained from VA or at http://www.va.gov/vaforms/. If you were separated after

January 1, 1950, you must submit DD Form 214, Certificate of Release or Discharge From Active

Duty.

Questions and Answers

1. Does active duty for training in the Guard and Reserves qualify a person for home loan

benefits?

No. Active duty for training in the Guard and Reserves does not qualify a person for home

loan benefits, unless the person completes a total of 6 years in the Guard and/or Reserves and

serves under title 10, U.S.C.

2. Does this kind of service provide entitlement to any other veterans’ home loan benefit?

Yes. Active-duty-for-training service may qualify you for a HUD/FHA veterans’ loan.

Under the National Housing Act loan program, the Federal Housing Administration of the

Department of Housing and Urban Development administers a loan program for veterans.

Financing under this program is available under slightly more favorable terms than those

available to nonveterans. VA’s only role in this program is to determine the eligibility of the

veteran and, if qualified, issue a Certificate of Veteran Status as evidence of entitlement to

HUD/FHA loan benefits for veterans.

You may get a Certificate of Veteran Status by completing VA Form 26-8261a, Request for

Certificate of Veteran Status, and submitting it with the attachments listed in the instructions to VA

for a determination of eligibility. This form may be obtained from VA or at

http://www.va.gov/vaforms/.

All veterans discharged under other than dishonorable conditions from at least 90 days of service

which began before September 8, 1980, are eligible. Veterans of enlisted service in a regular

component of the Armed Forces, which began after September 7, 1980, or officers or reservists

who entered on active duty after October 13, 1982, must have served at least 24 months of

service or the full period for which called to active duty or Active Duty for Training before being

discharged, unless the discharge was for hardship or disability.

3. What can a veteran do who has lost his or her original discharge papers and does not

have a legible copy?

The veteran should obtain a Certificate in Lieu of Lost or Destroyed Discharge. Any VA office will

assist the veteran in obtaining necessary proof of military service.

4. Does a veteran’s home loan entitlement expire?

No. Home loan entitlement is generally good until used. However, the eligibility of service

personnel is only available so long as they remain on active duty. If they are discharged or

released from active duty before using their entitlement, a new determination of their eligibility

must be made, based on the length of service and the type of discharge received.

5. How much entitlement does each veteran have?

Originally, the maximum entitlement available was $2,000; however, legislation enacted since

that time has provided veterans with increases in entitlement up to the present maximum of

$36,000 (or up to $ 89,912 for certain loans over $144,000). The $36,000 may, however, be

reduced if entitlement has been used before to get a VA loan. The amount of remaining

entitlement can be determined by subtracting the amount of entitlement used from the current

maximum available entitlement of $36,000. (See question 8 for information on using remaining

entitlement.)

6. Does VA home loan entitlement provide cash to the veteran?

No. The amount of entitlement relates only to the amount VA will guarantee the lender against

loss.

7. Can a veteran get used entitlement back to use again?

If you have used all or part of your entitlement, you can get that entitlement back to purchase

another home if the following conditions for “restoration” are met:

The property has been sold and the loan has been paid in full, or

A qualified veteran-transferee (buyer) must agree to assume the outstanding balance

on the loan and agree to “substitute” his or her entitlement for the same amount of

entitlement you originally used to get the loan. The buyer must also meet the occupancy

and income and credit requirements of the law.

ONE TIME ONLY if you have repaid the prior VA loan in full, but have not disposed of the

property securing that loan, the entitlement you used in connection with that loan may be

restored.

Any loss suffered by VA as a result of guaranty of the loan (for example a claim paid to a

lender if a loan goes to foreclosure) must be repaid in full before the entitlement used on the

loan can be restored.

Restoration of entitlement is not automatic. You must apply for it by completing and returning VA

Form 26-1880, “Request for a Certificate of Eligibility” to the Eligibility Center. This form may be

obtained from any VA office or at http://www.va.gov/vaforms/.

8. If the requirements for restoration cannot be met, is there any other way a veteran

can obtain another VA loan?

Yes. Veterans who had a VA loan before may still have “remaining entitlement” to use for

another VA loan. The current amount of entitlement available to each eligible veteran is $36,000

($89,912 for certain loans over $144,000). This was much lower in years past and has been

increased over time by changes in the law. For example, a veteran who obtained a $25,000 loan

in 1974 would have used $12,500 guaranty entitlement, the maximum then available. Even if that

loan is not paid off, the veteran could use the $23,500 difference between the $12,500

entitlement originally used and the current maximum of $36,000 to buy another home with VA

financing.

Most lenders require that a combination of the guaranty entitlement and any cash downpayment

must equal at least 25 percent of the reasonable value or sales price of the property, whichever is

less. Thus, in the example, the veteran’s $23,500 remaining entitlement would probably meet a

lender’s minimum guaranty requirement for a no-downpayment loan to buy a property valued at,

and selling for, $94,000. The veteran could also combine a downpayment with the remaining

entitlement for a larger loan amount.

9. May several veterans use their entitlement to acquire property together?

Yes. The guaranty is based on each veteran’s interest in the property, but the guaranty on the

loan may not exceed the lesser of 40 percent of the loan amount or $36,000 ($89,912 for certain

loans over $144,000).

10. If both a husband and wife are eligible, may they acquire property jointly and so

increase the amount which may be guaranteed?

They may acquire property jointly, but the amount of guaranty on the loan may not exceed the

lesser of 40 percent of the loan amount or $36,000 ($89,912 for certain loans over $144,000).

11. May a veteran join with a nonveteran in obtaining a VA loan?

Yes, but the guaranty is based only on the veteran’s portion of the loan. The guaranty cannot

cover the nonveteran’s part of the loan. This does not apply to a loan to a veteran and spouse

when the spouse is not a veteran. (Consult lenders to determine whether they would be willing to

accept applications for joint loans of this type.)

12. Does the issuance of a certificate of eligibility guarantee approval of a VA loan?

No. The veteran must still be found to be qualified for the loan from an income and credit

standpoint.

13. Can a veteran or active duty servicemember who is eligible for a Specially Adapted

Housing (SAH) grant apply for a GI home loan from a private lender to cover the

difference between the total cost of the house and the SAH grant?

Yes. A veteran or active duty servicemember who is eligible for a Specially Adapted Housing

(SAH) grant can apply for a GI home loan from a private lender to cover the difference between

the total cost of the house and the SAH grant. SAH program eligibility requirements and points of

contact information are available at http://www.benefits.va.gov/homeloans/sah.asp.

14. If private financing is not available, can VA make the veteran or active duty

servicemember a direct loan to cover the difference between the total cost of the house

and a Specially Adapted Housing (SAH) grant?

Yes, provided the veteran or active duty servicemember has GI home loan entitlement and

qualifies from a credit standpoint. The maximum direct loan is currently $33,000.

ELIGIBLE LOAN PURPOSES

You may use VA-guaranteed financing:

• To buy a home.

• To buy a townhouse or condominium unit in a project that has been approved by VA.

To build a home.

To repair, alter, or improve a home.

To simultaneously purchase and improve a home.

.

To improve a home through installment of a solar heating and/or cooling system or other

energy efficient improvements.

To buy a manufactured (mobile) home and/or lot.

To buy and improve a lot on which to place a manufactured home which you already

own and occupy.

To refinance a manufactured home loan in order to acquire a lot. (See VA Pamphlet 26-

71-1, which is available on the internet at: http://www.benefits.va.gov/homeloans/vap26-71-

1.asp, for more information about manufactured home loans.)

Questions and Answers

1. Can a veteran get a VA loan to pay off the mortgage or other liens of record on his or

her home?

Yes. The following refinancing loans are available under the VA-guaranteed home loan program:

To pay off the mortgage and/or other liens of record on the home. In most cases, the

loan may not exceed 90 percent of the reasonable value of the property as determined by

an appraisal, plus the funding fee, if required. The loan may include funds for any

purpose which is acceptable to the lender, plus closing costs, including a reasonable

number of discount points. A veteran must have available home loan entitlement. An

existing loan on a manufactured home (except as noted below) may not be refinanced

with a VA-guaranteed loan.

To refinance an existing VA loan to obtain a lower interest rate. Use of additional loan

entitlement is not required. The loan amount is limited to the balance of the old loan plus

the closing costs, discount points, funding fee, and up to $6,000 in energy efficient

improvements. An existing VA loan on a manufactured home may be refinanced to

obtain a lower interest rate.

2. Can a veteran get a VA business loan?

No, but business loans may be obtained through the SBA (Small Business Administration). The

SBA gives preference to veterans wishing to obtain small business assistance. For more

information on this financing, consult your telephone directory for the SBA office nearest you or

visit http://www.vetbiz.gov for general information on veterans in business.

3. Can a veteran get a VA farm loan?

No, except for a farm on which there is a farm residence which will be personally occupied by the

veteran as a home. The veteran may or may not conduct farming operations. If farming

operations are to be the primary source of the borrower’s income, then it must be established that

the venture has a reasonable likelihood for success. If the borrower plans to use the residence,

but has a source of income other than the farm which will be the primary source of income, then

the farming operations need not be considered. Other types of farm financing may be obtained

through the Farmers Home Administration which gives preference to veteran applicants.

Additional information can be obtained by contacting a local office of that agency, the address

and telephone number of which can be found in your telephone directory.

4. Can a veteran get a VA loan to buy or construct a residential property containing

more than one family unit?

Yes, but the total number of separate units cannot be more than four if one veteran is buying. If

more than one veteran is buying, then one additional family unit may be added to the basic four

for each veteran participating; thus, one veteran could buy four units; two veterans, six units;

three veterans, seven units, etc.

In addition, if the veteran must depend on rental income from the property to qualify for the loan,

the veteran must (a) show that he or she has the background or qualifications to be successful as

a landlord, and (b) have enough cash reserves to make the loan payments for at least 6 months

without help from the rental income.

5. Can a veteran get a VA loan to purchase a cooperatively-owned apartment?

VA is authorized to approve loans made to purchase a unit in a cooperative (co-op); however,

only a limited number of lenders have shown an interest in this type of loan.

6. Can a veteran obtain a VA loan for the purchase of property in a foreign country?

No. The property must be located in the United States, its territories, or possessions. The

territories and possessions are Puerto Rico, Guam, Virgin Islands, American Samoa, and

Northern Mariana Islands.

7. Can a veteran obtain a loan from a private lender in one State for the purchase of

property in another State?

Yes. However, many lenders limit their lending operations to certain areas.

8. May a lender require security from the veteran in addition to the property being

purchased?

Yes. This is a matter between the veteran and the lender. While VA does not require that

additional security be taken, it does not object if the veteran is willing.

APPLYING FOR THE LOAN

VA-guaranteed loans are obtained by making an application to private lending institutions.

Lenders may be found by asking in the community in which you live what firms in the area make

home loans. This information may be obtained from the local chamber of commerce, by looking

in the telephone directory under “Mortgages,” or by inquiring at banks, savings and loan

associations, mortgage companies, real estate brokers’ offices, and other public and private

lending agencies.

Most mortgage lenders will have the forms and other necessary papers to apply for a certificate of

eligibility and for the loan and will help you fill them out. Any lender who does not have the forms

may obtain them from VA.

If you have a certificate of eligibility, you should present it to your lender when making your loan

application, because the lender will want assurance that you are eligible before accepting the

application. However, a lender will undoubtedly discuss the possibility of making a VA loan to

you without seeing the certificate. In fact, many lenders will assist you in applying for a certificate

It is most important that you not make any commitments based on an expected approval of your

loan. You should not, for example, give notice to your landlord until the loan is actually approved

of eligibility. So, even if you have not obtained a certificate, you should not delay making an

application to a lender for a loan just for this reason.

To reduce delays in the processing of the loan, you should be prepared to give the lender the

complete names and addresses and your employee identification numbers for present and past

employers covering a 2-year period. You should also have available the location and account

numbers for savings and checking accounts and all open and recently closed debts and

obligations.

Questions and Answers

1. If a lender is unwilling to accept a veteran’s application for a loan, what should the

veteran do?

The veteran should see another lender. The fact that one lender is not interested in making the

loan the veteran wants does not mean that other lenders will not make the loan.

2. How are VA loans processed? There are two ways a lender may process VA

home loans: “prior approval” or “automatic.”

When the loan is processed on a prior approval basis, the lender takes your application, requests

VA to appraise the property, and verifies your income and credit record. All this information is put

together in a loan package and sent to VA for review. If VA approves the loan, a commitment by

VA to guarantee the loan is sent to the lender. The lender then closes the loan and sends a

report of the closing to VA. If the loan complies with VA requirements, VA issues the lender a

certificate of guaranty.

In automatic processing, the lender still orders an appraisal from VA, but has the authority to

make the credit decision on the loan without VA’s approval. The biggest difference between prior

approval and automatic processing is the time saved by avoiding the need to await VA’s approval

before loan closing.

All lenders do not have the authority to process loans on the automatic basis. Banks, savings

and loan associations, and certain other lenders such as mortgage companies which are

approved by VA, have the privilege of processing VA-guaranteed loans using the automatic

procedure.

Lenders approved to participate in VA’s Lender Appraisal Processing Program (LAPP) are

generally able to expedite the processing of VA appraisals.

3. What should a veteran do while waiting for loan approval?

Sometimes it may take longer than you might expect for the lender or VA to process your loan

application. For instance, your current or former employer may be slow in returning an

employment verification form, or it may take some time to obtain a credit rating from out-of-State

creditors.

Occasionally, the application VA receives from the lender is incomplete in some important aspect

and requires that VA ask the lender to furnish additional information before a final decision can be

made. Ordinarily, you should plan on an average of 4 to 6 weeks to obtain a decision on your

application.

In any case, information on the progress of your application should be obtained from the lender,

who will be most aware of developments as they occur.

by VA (or by your lender if the automatic processing procedure is used). Generally, it is not

advisable to move into the home before the loan is approved. If for some reason the loan is not

obtained, you could be faced with additional expense and inconvenience.

4. What is pre-purchase counseling and why would it be helpful?

Pre-purchase counseling is especially helpful to a first time homebuyer. It gives a person useful

information on (1) the process of buying a home, (2) the key players in the home buying process

and (3) debt management. The goal is to create a more well informed homebuyer. While VA

does not require such counseling, we strongly recommend it. There is usually no charge for the

housing counseling. To locate a housing counseling office, call (800) 569-4287. This is a

Department of Housing and Urban Development (HUD) maintained number and referral service.

LOAN REPAYMENT TERMS

The maximum VA home loan term is 30 years and 32 days; however, the term may never be for

more than the remaining economic life of the property as determined by the appraisal.

Questions and Answers

1. May a veteran pay off a VA loan before it becomes due?

Yes. A VA loan may be partially or fully paid at any time without penalty. Partial payments may

not be less than 1 monthly installment or $100, whichever is less. (Consult your lender.)

2. May the maturity on a VA loan be extended to reduce the monthly payments?

Yes, provided the veteran and the lender want to extend it and the extension provides for

complete repayment of the loan within the maximum period permitted for loans of its type.

3. If a veteran dies before the loan is paid off, will the VA guaranty pay off the balance

of the loan?

No. The surviving spouse or other coborrower must continue to make the payments. If there is

no coborrower, the loan becomes the obligation of the veteran’s estate. Protection against this

may be obtained through mortgage life insurance, which must be purchased from private

insurance sources.

4. Will the veteran’s payments always be paid to the same company?

No. It is common practice in the mortgage lending industry to sell mortgages, often before the

first payment is even due. If your loan is sold, you may find that you sent your first payment to

the wrong place and the new holder of your loan may send you an overdue notice. Even though

you know you made the payment, and it is up to the two lenders to get it straightened out, do not

ignore the notice. (Most lenders will notify the veteran if the loan is sold and help straighten out

any problems.)

5. Does having a VA loan limit a veteran’s right or ability to sell the property?

No. A veteran may sell the property to a veteran or nonveteran at any time. However, if the loan

was approved on or after March 1, 1988, and it will be assumed, the qualifications of the assumer

must be reviewed and approved by the lender or VA.

6. When a veteran sells the property to someone who will assume the existing VA loan,

is the veteran released automatically from personal liability for repayment of the loan?

No. If the loan was approved on or after March 1, 1988, the lender or VA must be notified and

It is most important that you not make any commitments based on an expected approval of your

loan. You should not, for example, give notice to your landlord until the loan is actually approved

requested to approve the assumer and grant the veteran release from liability. If the loan was

approved prior to March 1, 1988, the loan may be assumed without approval from VA or the

lender. However, the veteran is strongly urged to request a release of liability from VA.

7. If a loan closed prior to March 1, 1988 can be assumed without VA’s approval, why

should a veteran be concerned about requesting and obtaining a release from

personal liability?

If a veteran does not obtain a release of liability, and VA suffers a loss on account of a default by

the assumer or some future assumer, a debt may be established against the veteran. Also,

strenuous collection efforts will be made against the veteran if a debt is established.

8. How may a veteran obtain a release of liability from VA?

By having the buyer assume all of the veteran’s liabilities on the VA loan, and by having VA or the

loan holder approve the buyer and the assumption agreement. If the VA loan was approved prior

to March 1,1988, the application forms for a release of liability must be requested from the VA

Regional Loan Center of Jurisdiction. In most cases, if the VA loan was approved on or after

March 1, 1988, the application forms must be requested from the lender to whom the payments

are made.

9. If a veteran obtains a release of liability, is restoration of entitlement automatic?

No. Restoration requirements may be found in the above information.

REPAYMENT PLANS

VA will guarantee loans to purchase homes made with the following repayment plans:

Traditional Fixed-Payment Mortgage

This type of mortgage loan calls for equal monthly payments for the life or term of the

loan. Each monthly payment reduces a certain portion of the principal owed on the loan

and pays interest accrued to date.

GPM (Graduated Payment Mortgage)

This repayment plan provides for smaller-than-normal monthly payments for the first few

years (usually 5 years), which gradually increase each year, and then level off after the

end of the “graduation period” to larger-than-normal payments for the remaining term of

the loan. The reduction in the monthly payment in the early years of the loan is

accomplished by delaying a portion of the interest due on the loan each month and by

adding that interest to the principal balance.

Buydowns

The builder of a new home or seller of an existing home may “buy down” the veteran’s

mortgage payments by making a large lump-sum payment up front at closing that will be

used to supplement the monthly payments for a certain period, usually 1 to 3 years.

GEM (Growing Equity Mortgage)

This repayment plan provides for a gradual annual increase in the monthly payments with

all of the increase applied to the principal balance. The annual increases in the monthly

payment may be fixed (for example, 3 percent per year) or tied to an appropriate index.

The increases to the monthly payment result in an early payoff of the loan in about 11 to

16 years for a typical 30 year mortgage.

ARM (Adjustable Rate Mortgages)

FUNDING FEE

ARM loans are typically made at an initial interest rate lower than market rate; however

the interest rate can be adjusted – up or down – during the life of the loan. A one year

ARM allows for annual adjustments of no more than 1percent and a lifetime cap of 5

percent. Hybrid ARM loans allow for an initial fixed rate for a period of at least 3 years,

followed by annual adjustments. Depending on the length of the fixed rate period, the

initial adjustment can be up to 2 percent and the lifetime cap is either 5 percent or 6

percent.

DOWNPAYMENT REQUIREMENTS

Traditional Fixed-Payment Mortgage, Buydown Loans, and Growing Equity Mortgage

VA does not require a downpayment if the purchase price or cost is not more than the

reasonable value of the property as determined by VA, but the lender may require one. If

the purchase price or cost is more than the reasonable value, the difference must be paid

in cash from your own resources.

Graduated Payment Mortgage

The maximum loan amount may not be for more than the reasonable value of the property

or the purchase price, whichever is less. Because the loan balance will be increasing

during the first years of the loan, a downpayment is required to keep the loan balance

from going over the reasonable value or the purchase price.

INTEREST RATES

The interest rate on VA loans can be negotiated based on prevailing rates in the mortgage

market. Once a loan is made, the interest rate set in the note will stay the same for the life of the

loan.

However, if interest rates go down, and you still own and occupy (or previously occupied) the

property securing a previous VA loan, you may apply for a new VA loan to refinance the previous

loan at a lower interest rate without using any additional entitlement.

CLOSING COSTS

The cost of obtaining any mortgage can be quite a lot. VA regulates those closing costs that a

veteran may be charged in connection with closing a VA loan. No commission or brokerage fees

may be charged to you for obtaining a VA loan. However, you may pay reasonable closing costs

to the lender in connection with a VA-guaranteed loan.

Although some additional costs are unique to certain localities, the closing costs generally include

VA appraisal, credit report, survey, title evidence, recording fees, a 1 percent loan origination fee,

and discount points. The closing costs and origination charge may not be included in the loan,

except in VA refinancing loans.

In addition to negotiating the interest rate with the lender, veterans may negotiate the payment of

discount points and other closing costs with the seller.

Often, sellers will consider paying some or all of the discount points required by the lender in

order to complete the sale. This can have a big impact on the amount of cash you must pay out

of pocket in order to complete the purchase. If the seller will not consider paying points, the

veteran may be able to negotiate an interest rate with the lender which is sufficient to avoid the

need to include any discount points in the transaction.

Therefore, if you are seeking to use your entitlement to buy a home, you may be assured that VA

will protect your civil rights and equal housing opportunity.

Veterans must also pay a VA funding fee at the time of loan closing. The fee may be included in

the loan and paid from loan proceeds. The fee is not required from veterans in receipt of service-

connected compensation, or who would be but for receipt of military retired pay, or surviving

spouses of veterans who died in service or from service-connected causes.

Joel Lobb

Mortgage Loan OfficerIndividual NMLS ID #57916

American Mortgage Solutions, Inc.

Company NMLS ID #1364

click here for directions to our office

Text/call: 502-905-3708

fax: 502-327-9119

email: kentuckyloan@gmail.com

You must be logged in to post a comment.