Are you a veteran, active-duty service member, or eligible spouse in Kentucky looking to secure a VA mortgage loan? Joel Lobb, a seasoned mortgage broker, provides valuable insights into what it takes to qualify for a VA loan, covering credit score, bankruptcy, work history, debt-to-income ratio, foreclosure, income limits, loan limits, appraisal requirements, termite requirements, and type of residence. Let’s dive into the details:

Qualifying for a VA Mortgage Loan in Kentucky: A Comprehensive Guide by Joel Lobb

Are you a veteran, active-duty service member, or eligible spouse in Kentucky looking to secure a VA mortgage loan? Joel Lobb, a seasoned mortgage broker, provides valuable insights into what it takes to qualify for a VA loan, covering credit score, bankruptcy, work history, debt-to-income ratio, foreclosure, income limits, loan limits, appraisal requirements, termite requirements, and type of residence. Let’s dive into the details:

Qualification Criteria Requirements

Credit Score

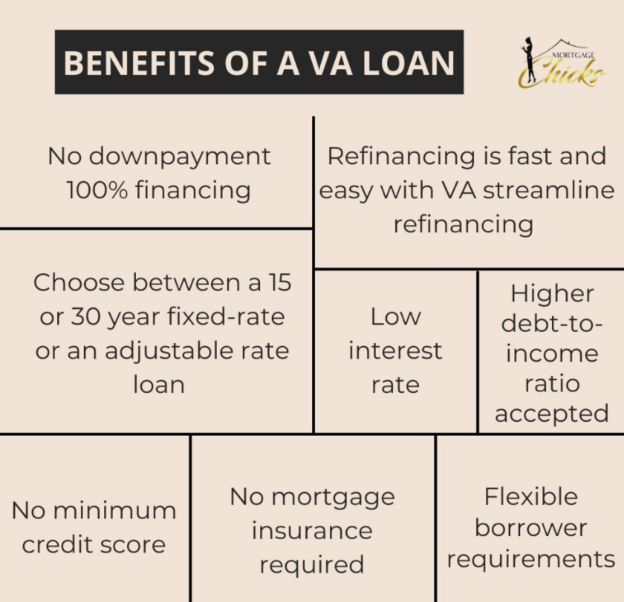

While there is no official minimum credit score requirement, most lenders prefer a score of 620 or higher.

Bankruptcy

Chapter 7 bankruptcy: Generally, two years must have passed since the discharge date.

Chapter 13 bankruptcy: Typically, one year of on-time payments and approval from the bankruptcy court are required.

Work History

Stable employment history with at least 2 years of continuous employment or income sources.

Debt-to-Income Ratio (DTI)

Maximum total debt-to-income ratio typically ranges from 41%, depending on the lender and other factors.

Foreclosure

Generally, two years must have passed since the foreclosure date.

Income Limits

VA loans do not have specific income limits, but income must be sufficient to cover monthly expenses and qualify for the loan amount.

Loan Limits

VA loan limits vary by county in Kentucky. Joel Lobb can provide information on the specific limits for your area.

Appraisal Requirements

The property must undergo a VA appraisal to assess its value and ensure it meets VA standards.

Termite Requirements

A termite inspection may be required for properties in certain areas prone to termite infestation.

Type of Residence

VA loans can be used to finance primary residences, including single-family homes, condos, and certain multi-unit properties.

Joel Lobb understands the nuances of VA mortgage loans and can guide you through the qualification process with expertise and personalized attention. Contact Joel Lobb today to learn more about VA loans in Kentucky and take the first step towards securing your dream home.

Joel Lobb understands the nuances of VA mortgage loans and can guide you through the qualification process with expertise and personalized attention. Contact Joel Lobb today to learn more about VA loans in Kentucky and take the first step towards securing your dream home.

Joel Lobb Mortgage Loan Officer

American Mortgage Solutions, Inc.

10602 Timberwood Circle

Louisville, KY 40223

Company NMLS ID #1364

Text/call: 502-905-3708

fax: 502-327-9119

email: kentuckyloan@gmail.com

http://www.mylouisvillekentuckymortgage.com/

NMLS 57916 | Company NMLS #1364/MB73346135166/MBR1574

The view and opinions stated on this website belong solely to the authors, and are intended for informational purposes only. The posted information does not guarantee approval, nor does it comprise full underwriting guidelines. This does not represent being part of a government agency. The views expressed on this post are mine and do not necessarily reflect the view of my employer. Not all products or services mentioned on this site may fit all people.

NMLS ID# 57916, (www.nmlsconsumeraccess.org).