|

||

|

Leave a reply

|

||

|

If you’re considering buying a home in Kentucky and looking for a mortgage loan with favorable terms, a Kentucky USDA loan could be a great option. Kentucky USDA loans, backed by the U.S. Department of Agriculture, are designed to help low to moderate-income borrowers in Kentucky rural areas achieve homeownership. Here’s a comprehensive guide on how to get approved for a USDA mortgage loan in Kentucky in regards to credit score, income, work history, debt to income ratios, bankruptcy and foreclosure :

To get a Kentucky USDA loan, potential Kentucky rural housing borrowers must follow this sequence of steps:

Keep in mind that you’ll have fees associated with your loan. Guaranteed loans require an upfront 1% fee and annual fees of 0.35% for as long as the mortgage is active.

USDA program for properties located outside urban areas of Kentucky areas where you can secure a no money down loan at a fixed rate of on 30 years.

The max household income limits usually are between $110,500 to $146,000 for most rural area counties depending on household family size.

This changes every year so make sure you are using updated USDA Income Limits for this year

A 620-640 middle credit score is needed for loan approval on this program. They’re no max loan limits on USDA loans. You just need to qualify based on your debt to income ratio (see below under income section)—–USDA will go down to 580 on scores but it has to pass USDA Manual Underwriting guidelines

Need to be 3 years removed from a Chapter 7 Bankruptcy and 3 years from a foreclosure

Joel Lobb Mortgage Loan Officer

American Mortgage Solutions, Inc.

10602 Timberwood Circle

Louisville, KY 40223

Text/call: 502-905-3708

fax: 502-327-9119

email: kentuckyloan@gmail.com

http://www.mylouisvillekentuckymortgage.com/

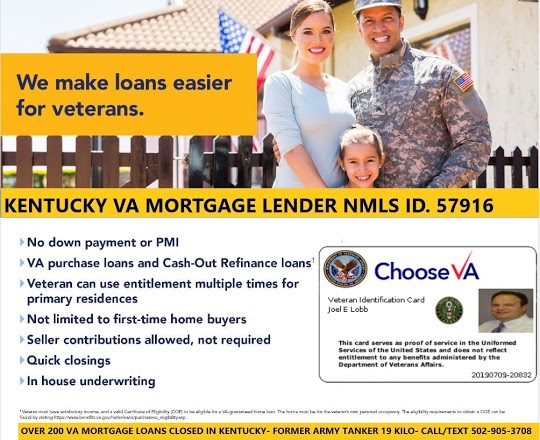

When comparing Kentucky VA loans to Kentucky USDA, FHA, and Fannie Mae loans in Kentucky, several factors come into play, including credit score requirements, income considerations, work history, debt ratios, and how each loan type treats bankruptcy and foreclosure. Let’s delve into the benefits and differences of each loan type:

Kentucky Mortgage Credit Score Requirements:

Kentucky Mortgage Income and Work History:

Kentucky Mortgage Debt Ratio Requirements:

Kentucky Mortgage Bankruptcy and Foreclosure Requirements:

Advantages and Disadvantages of Kentucky VA loans, USDA, Fannie Mae and FHA:

In summary, choosing the right loan type depends on your specific financial situation, eligibility criteria, and property location. VA loans offer excellent benefits for eligible veterans and service members, while USDA, FHA, and Fannie Mae loans provide alternatives with their own advantages and considerations.

American Mortgage Solutions, Inc.

10602 Timberwood Circle

Louisville, KY 40223

Company NMLS ID #1364

Text/call: 502-905-3708

fax: 502-327-9119

email: kentuckyloan@gmail.com

http://www.mylouisvillekentuckymortgage.com/

The view and opinions stated on this website belong solely to the authors, and are intended for informational purposes only. The posted information does not guarantee approval, nor does it comprise full underwriting guidelines. This does not represent being part of a government agency. The views expressed on this post are mine and do not necessarily reflect the view of my employer. Not all products or services mentioned on this site may fit all people.

NMLS ID# 57916, (www.nmlsconsumeraccess.org).