How can I get a VA Mortgage loan in Kentucky in 2021?

Kentucky veterans and active duty service members are eligible. However, all veterans, active duty service members and National Guard members must meet certain requirements.

see below requirements for Kentucky VA Mortgage Loans:

- Served 90 consecutive days during wartime

- Served 181 days during peacetime

- Have more than six years of service with the National Guard or Reserves

Also, Kentucky VA loans are available to the surviving spouses of military members who died in the line of duty.

How does a Kentucky VA Home Mortgage Loan Work?

The Veterans Administration guarantees the loan, but they do not make it.. VA sets forth the guidelines as far as credit, income, assets, property requirements and inspections, but the lenders use this to make a lending decision. Usually the credit, income and assets, i.e. bank statements, pay stubs and tax returns, along with credit report and credit score to get a pre-approval upfront. The appraisal report is done by VA assigned appraiser in the area and neither the lender, borrower, realtors, sellers, have no control as far as choosing the Kentucky VA appraiser. VA will typically give the VA approved appraiser 10 days to make contact, and usually get the appraisal report back within 7-10 days after inspections.

How much can I borrow with a Kentucky Mortgage VA loan?

There is no max income limit for VA loans beginning in 2021.

VA Loan Limits in Kentucky for 2021

VA does not set a cap on how much you can borrow to finance your home. However, there are limits on the amount of liability VA can assume, which usually affects the amount of money an institution will lend you. The loan limits are the amount a qualified Veteran with full entitlement may be able to borrow without making a down-payment. These loan limits vary by county, since the value of a house depends in part on its location.

The basic entitlement available to each eligible Veteran is $36,000. Lenders will generally loan up to 4 times a Veteran’s available entitlement without a down payment, provided the Veteran is income and credit qualified and the property appraises for the asking price.

VA county loan limit:

- VA’s 2021 Loan Limits are the same as the Federal Housing Finance Agency’s limits – 2021 Loan Limits (Effective January 1, 2020).

For all non-IRRRL VA loans, effective with loans closed on or after January 1, 2021, we are aligning with FHFA’s increase to the county loan limits. VA does not have a maximum loan amount, but instead uses the county loan limit to determine the maximum potential entitlement available for veterans with used or compromised entitlements.

Complete details of Kentucky VA’s county loan limits can be found at

https://www.va.gov/housing-assistance/home-loans/loan-limits/.

As a reminder, we require that all Kentucky VA loans conform to GNMA secondary market guidelines which include the minimum 25% coverage requirement.

What is the credit score or fico score required for a Kentucky VA Mortgage loan?

VA has issued guidelines that calls for no minimum credit score. However, most VA Kentucky lenders will want to see a credit score of at least 620 before approving the mortgage. There are two lenders we work with currently that will do down to a 500 credit score, but it is very difficult to get them approved . The best thing to do is let someone pull your credit and see where you are at and go from there. A lot of lenders you will see will want a 620 credit score, with a few going down to 580. Again, this will vary greatly from lender to lender and be based upon our automated underwriting findings (AUS) from Desktop Underwriting.

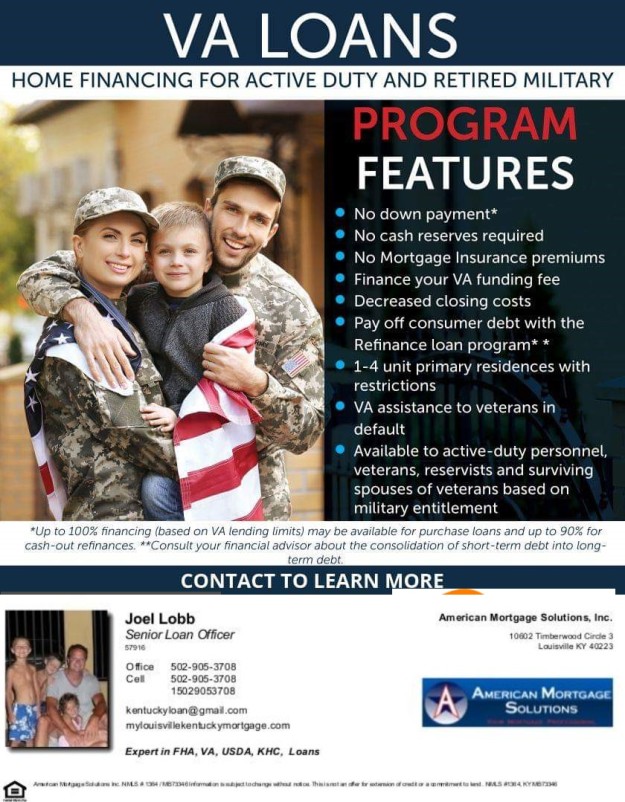

Do VA Loans Require a Down payment.

Kentucky VA home buyers do not require a down payment. It does not matter if you have a 500 credit score or 780 credit score, all VA loans offer a no down payment option to applicants. The only reason you would need a down payment is if you had to qualify for the home loan payment, or if you were borrowing with a co-applicant, that is not married to the borrower. For example, if a veteran is legally married, and his wife is not a veteran, that is fine with VA and you would not need a down payment, However, let’s say the borrower and his friend or girlfriend wanted to buy a house together, and we needed the co-borrowers income and credit to make it work, then you would need to put down 12% on the home loan since the borrower and co-borrower are not legally married.

Mortgage insurance on A VA loan?

One of the great benefits of VA loans is that have no monthly mortgage insurance premium. When you compare this to FHA, USDA mortgage loans in Kentucky, you would need to pay monthly mortgage insurance.

There is an upfront funding fee from VA , but if you are disabled, you can get this waived sometimes. See chart below

Kentucky VA Funding Fee Information

In order for VA to guarantee the home loan, there is a closing cost assessed by the VA to originate the loan called a funding fee. This fee will vary, depending upon the type of Kentucky VA loan, whether this is your first time to use your entitlement, if you are a disabled veteran, the down payment and if you served active duty or in the National Guard/Reserves.

How long does it take to close a VA Mortgage loan in Kentucky?

There’s no set-in-stone time limit for how long the Kentucky VA loan process takes, but on average, you should be able to get it done within 30 days depending on the appraisal report and home inspections

VA mortgage loans is the only Government sponsored mortgage that requires a termite inspection., so keep that in mind on your inspections when you are having them done after the accepted contract.

Can I only use a VA loan once in Kentucky?

This is a common myth with many VA eligible home buyers and homeowners. If you’re eligible for the VA loan, then you’re eligible for your entire life. Plenty of home buyers end up using the VA loan more than once, mostly because it’s arguably the best loan program out there.

Can I get a Kentucky VA Mortgage loan with a previous Bankruptcy or Foreclosure?

- If the applicant has finished making all payments satisfactorily, the lender may conclude that the applicant has reestablished satisfactory credit

- If the applicant is still in the repayment period, as long as 12 months’ worth of satisfactory payments have been made and the trustee or Bankruptcy Judge approves of the new credit, the lender may give favorable consideration.

- 2 years from discharge date

- Manual underwrites allowed

- If the bankruptcy was discharged within 1 to 2 years, it is probably not possible to determine that the applicant is a satisfactory credit risk unless both of the following requirements are met

- The applicant has obtained credit subsequent to the bankruptcy and has made satisfactory payments over a continued period of time, and

- The bankruptcy was caused by circumstances beyond the control of the applicant such as unemployment, prolonged strikes, medical bills not covered by insurance and the circumstances are verified. Divorce is not viewed as a circumstance beyond the applicants control

You must be logged in to post a comment.